IRS and LDR Provide Relief to Francine Victims in All of Louisiana: Various Deadlines Postponed to Feb. 3, 2025

The Internal Revenue Service announced tax relief for individuals and businesses in the entire state of Louisiana affected by Tropical Storm Francine that began on Sept. 10, 2024.

These taxpayers now have until Feb. 3, 2025, to file various federal individual and business tax returns and make tax payments.

The IRS is offering relief to any area designated by the Federal Emergency Management Agency (FEMA). This means that individuals and households that reside or have a business, anywhere in Louisiana, qualify for tax relief. The current list of eligible localities is always available on the Tax relief in disaster situations page on IRS.gov.

Filing and payment relief

The tax relief postpones various tax filing and payment deadlines that occurred from Sept. 10, 2024, through Feb. 3, 2025 (postponement period). As a result, affected individuals and businesses will have until Feb. 3, 2025, to file returns and pay any taxes that were originally due during this period.

This means, for example, that the Feb. 3, 2025, deadline will now apply to:

Any individual, business or tax-exempt organization that has a valid extension to file their 2023 federal return. The IRS noted, however, that payments on these returns are not eligible for the extra time because they were due last spring before the storm occurred.

Quarterly estimated income tax payments normally due on Sept. 16, 2024, and Jan. 15, 2025.

Quarterly payroll and excise tax returns normally due on Oct. 31, 2024, and Jan. 31, 2025.

In addition, penalties for failing to make payroll and excise tax deposits due on or after Sept. 10, 2024, and before Sept. 25, 2024, will be abated, as long as the deposits are made by Sept. 25, 2024.

The Disaster assistance and emergency relief for individuals and businesses page has details on other returns, payments and tax-related actions qualifying for relief during the postponement period.

The IRS automatically provides filing and penalty relief to any taxpayer with an IRS address of record located in the disaster area. These taxpayers do not need to contact the agency to get this relief.

It is possible an affected taxpayer may not have an IRS address of record located in the disaster area, for example, because they moved to the disaster area after filing their return. In these unique circumstances, the affected taxpayer could receive a late filing or late payment penalty notice from the IRS for the postponement period. The taxpayer should call the number on the notice to have the penalty abated.

In addition, the IRS will work with any taxpayer who lives outside the disaster area but whose records necessary to meet a deadline occurring during the postponement period are located in the affected area.

Taxpayers qualifying for relief who live outside the disaster area need to contact the IRS at 866-562-5227. This also includes workers assisting the relief activities who are affiliated with a recognized government or philanthropic organization.

Additional tax relief

Individuals and businesses in a federally declared disaster area who suffered uninsured or unreimbursed disaster-related losses can choose to claim them on either the return for the year the loss occurred (in this instance, the 2024 return normally filed next year), or the return for the prior year (the 2023 return filed this year). Taxpayers have extra time – up to six months after the due date of the taxpayer’s federal income tax return for the disaster year (without regard to any extension of time to file) – to make the election. For individual taxpayers, this means Oct. 15, 2025. Be sure to write the FEMA declaration number 3614-EM on any return claiming a loss. See Publication 547, Casualties, Disasters, and Thefts for details.

Qualified disaster relief payments are generally excluded from gross income. In general, this means that affected taxpayers can exclude from their gross income amounts received from a government agency for reasonable and necessary personal, family, living or funeral expenses, as well as for the repair or rehabilitation of their home, or for the repair or replacement of its contents. See Publication 525, Taxable and Nontaxable Income for details.

Additional relief may be available to affected taxpayers who participate in a retirement plan or individual retirement arrangement (IRA). For example, a taxpayer may be eligible to take a special disaster distribution that would not be subject to the additional 10% early distribution tax and allows the taxpayer to spread the income over three years. Taxpayers may also be eligible to make a hardship withdrawal. Each plan or IRA has specific rules and guidance for their participants to follow.

The IRS may provide additional disaster relief in the future.

The tax relief is part of a coordinated federal response to the damage caused by these storms and is based on local damage assessments by FEMA. For information on disaster recovery, visit disasterassistance.gov.

To view this original IRS article in its entirety and for more resources, please click here.

Louisiana Department of Revenue Grants Relief

In addition, in accordance with La. R.S. 47:1514(B) and (C), the Secretary of the Louisiana Department of Revenue (“LDR”) is granting filing and payment extensions to taxpayers whose homes, principal places of business, critical tax records or paid tax preparers are located in the federally declared disaster areas following Hurricane Francine.

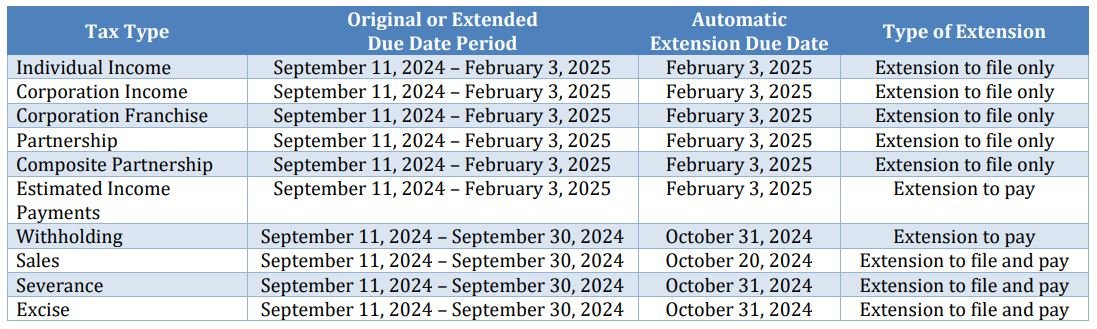

This chart is a summary of the extended Louisiana due dates for various tax types. Click on the image below to be taken to the full Revenue Information Bulletin:

As always, we are here to assist you however we can. If you have any questions about the deadline extension and how it affects you, please reach out to us and we will be happy to help.